¶ TAX GIVEAWAY

Highlights:

- Donald Trump’s tax bill was filled with corporate giveaways

- Corporate tax revenue crashed under the Tax Cuts and Jobs Act (TCJA).

- The TCJA’s direct corporate tax cut went to shareholders and the wealthiest.

- Corporations used the tax cuts to give more money to their shareholders.

- The TCJA’s corporate tax cuts propped up big banks.

- After the TCJA, business spending and corporate investment dropped to the lowest decline since 2009.

- Following the TCJA, corporations failed to make their promised investments.

- Non-real estate specific provisions in the TCJA benefitted corporations and the wealthy.

- The TCJA included carve outs for real estate holdings.

- Following the enactment of the TCJA, 91 corporations paid nothing in federal income taxes.

- Bonuses touted after the TCJA passed were one-time and insignificant compared to the shareholder returns.

- The TCJA was expected to add at least $1.9 trillion to the national debt over 10 years.

- The TCJA raised taxes on children of deceased service members and students receiving financial aid.

- The TCJA provided extensive benefits to the rich.

- Enough of the TCJA’s benefits flowed to the richest Americans to make the tax code no longer progressive at extreme income levels.

- The TCJA doubled the estate tax exemption, which saved the largest 1,800 estates $4.4 million each.

- The TCJA’s child tax credit skewed towards the wealthiest.

- More than a million military members would be forced to participate in Donald Trump’s payroll tax deferral and then pay that money back in 2021.

- Donald Trump campaigned on making the 2017 TCJA tax cuts permanent.

- Donald Trump planned a large corporate tax cut in a second term.

- Donald Trump’s economic team proposed cutting payroll taxes and instituting a flat tax in a second term.

Trump’s Tax Bill Was Filled With Corporate Giveaways

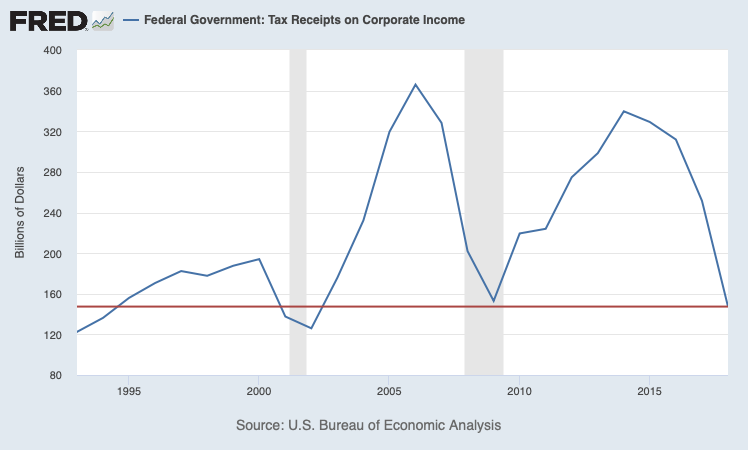

CORPORATE TAX REVENUE CRASHED UNDER THE TAX CUTS AND JOBS ACT (TCJA)

2018: Following The Passage Of The TCJA, Federal Government Corporate Tax Revenue Declined To The Nominal Lowest Level Since 2002.

[Federal Reserve Bank of St. Louis, accessed 1/27/20]

2018: Corporate Tax Revenues Fell By 31%, Almost Twice Official Budget Projections For Trump Tax Cuts. According to Politico, “Federal tax payments by big businesses are falling much faster than anticipated in the wake of Republicans’ tax cuts, providing ammunition to Democrats who are calling for corporate tax increases. The U.S. Treasury saw a 31 percent drop in corporate tax revenues last year, almost twice the decline official budget forecasters had predicted. Receipts were projected to rebound sharply this year, but so far they’ve only continued to fall, down by almost 9 percent or $11 billion.” [Politico, 6/13/19]

- The Only Times Corporate Tax Revenues Have Been As Small A Share Of GDP Since 1965 Came During Recessions. According to Politico, “Overall corporate revenues last year amounted to 1 percent of GDP, a level they’ve dipped to only twice since 1965. Both of those previous instances, in 2009 and 1983, came in the wake of recessions, when business profits had cratered.” [Politico, 6/13/19]

FY 2019: Tax Revenue Was $225 Billion Less Than It Was Projected To Be In 2017 Before Trump’s Tax Cuts. According to the Washington Examiner, “After two years, President Trump's tax cuts are not on track to pay for themselves, the latest Treasury data released Friday suggest. Total federal government revenues ended up lower in 2019 than was projected before the passage of the GOP tax overhaul in 2017. Then, in 2017, the nonpartisan Congressional Budget Office projected that fiscal 2019 revenues, without the tax cuts, would be $3.69 trillion. Instead, revenues with the tax cuts were only $3.46 trillion. To be certain, the difference, $225 billion, cannot be attributed solely to the tax cuts. Other economic factors have influenced economic growth over the past two years. For example, the tariffs put in place as part of Trump's trade wars likely counteracted the stimulative [sic] effect of the tax cuts.” [Washington Examiner, 10/26/19]

FY 2020: The CBO Cut Projections For Corporate Tax Revenue By $11 Billion As Corporate Profits Are Expected To Come In Lower Than Anticipated. According to Politico Pro, “The Congressional Budget Office is cutting its estimate of how much corporations will pay in total taxes this year. In a biannual report on the government’s finances, the nonpartisan agency said today it expects corporate receipts this year to come in at $234 billion. That’s down four percent from the $245 billion it had predicted in August, and would be up slightly from 2019’s actual total of $230 billion. Tax payments by big businesses have been a touch issues since Republicans slashed the corporate rate as part of their 2017 tax cuts. CBO said there were crosscutting trends but that a big factor for the reduced projection is its expectation that corporate profits will be lower than anticipated. [Politico Pro, 1/28/20]

THE TCJA’S DIRECT CORPORATE TAX CUT WENT TO SHAREHOLDERS AND THE WEALTHIEST

The TCJA Cut The Corporate Tax Rate From 35% To 21. According to Vox, “The tax law’s centerpiece is its record cut in the corporate tax rate, from 35 percent to 21 percent.” [Vox, 1/24/20]

Corporations Used The Tax Cut To Give More Money To Their Shareholders

Companies Used The Corporate Tax Cut To Give Money To Their Shareholders. According to Vox, “The tax law’s centerpiece is its record cut in the corporate tax rate, from 35 percent to 21 percent. At the time of its passage, most of the bill’s Republican supporters said the cut would result in higher wages, factory expansions, and more jobs. Instead, it was mainly exploited by corporations, which bought back stock and raised dividends.” [Vox, 01/24/20]

Many Private Equity Firms Reformed To Get In On The Corporate Rate Cuts

Despite The TCJA’s 20% Deduction For Pass-Through Businesses, Many Private Equity Firms Converted To C-Corps Because The Corporate Rate Was Cut So Significantly. According to the Geraci Law Firm, “In the real estate and lending industry, one of the more popular statutory provisions within TCJA is the 20% QBI deduction for real estate investment trusts (‘REITs’). The other area where it is gaining traction is the conversion of entities from partnerships to C-corporations due to the tax rate dropping from 35% to 21%. Several publicly traded private equity firms are making the jump to convert their businesses, most notably, Apollo Global Management LLC and KKR & Co LP.” [Geraci Law Firm, 9/23/19]

Following The Enactment Of The TCJA, The Median Effective Global Tax Rates For Companies Fell

Since The Enactment Of The Tax Cuts And Jobs Act, The Median Effective Global Tax Rate For S&P 500 Companies Has Fallen From 25.5% To 19.8%. According to the Wall Street Journal, “The U.S. tax overhaul has lowered tax rates for many companies, and many others that were already toward the bottom of the scale have been able to stay there so far, a Wall Street Journal analysis shows. The lower rates follow tax-law changes Congress passed at the end of 2017. Since then, the Journal analysis shows, the median effective global tax rate for S&P 500 companies declined to 19.8% in the first quarter of 2019 from 25.5% two years earlier. That marked the third straight quarter below 20% and is consistent with the goals and structure of the tax overhaul, which lowered the federal corporate rate to 21% from 35%. The law’s authors wanted to help U.S. multinationals compete in foreign markets and aid domestic companies with high tax burdens, while reducing the value of tax breaks and making it harder to achieve single-digit tax rates.” [Wall Street Journal, 7/21/19]

Wall Street Journal: Q2 2018 – Q2 2019: S&P 500 Companies Paid A Global Effective Tax Rate Lower Than 20%, Despite The Fact That The U.S. Corporate Tax Rate Is 21% Thanks To “A Variety Of Tax Breaks.” According to the Wall Street Journal, “Companies typically don’t make public what they pay the Internal Revenue Service each tax year. But public companies do disclose their effective tax rates: the measure of taxes incurred under generally accepted accounting principles as a share of pretax income. Those rates reflect global results and include foreign and state taxes, not just what companies owe the U.S. Treasury Department. Quarterly results can bounce around, swayed by one-time events. For many big companies, however, U.S. federal taxes are the most important component. A quarter of S&P 500 companies reported effective global tax rates below 21% in each of the past four quarters, the Journal analysis found. Companies can wind up paying less than the statutory rate, even on U.S. income, thanks to a variety of breaks that lower their tax bills, including a deduction for exports and credits for corporate research. The Journal’s analysis, using figures from financial-data firm Calcbench Inc., omits tax rates reported for the last three months of 2017 and the first three months of 2018—quarters in which many companies booked big, one-time changes driven by the tax law. Results were similar when real-estate companies, which tend to report very low tax rates, were omitted. (See methodology note for more detail.) A separate analysis, from S&P Dow Jones Indices, found similar shifts in income-tax rates for S&P 500 companies since the tax law’s enactment.” [Wall Street Journal, 7/21/19]

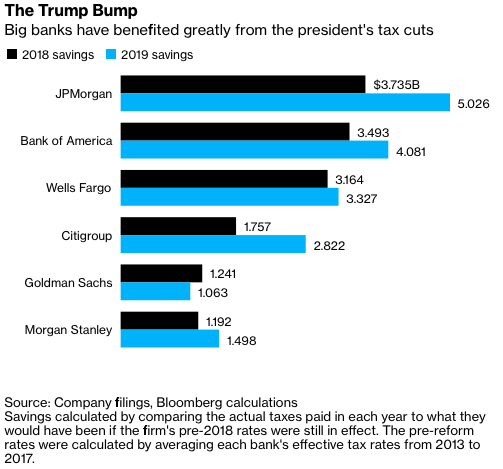

The TCJA Propped Up Big Bank Earnings

Q1 2019 – Q2 2019: Bank Of America, Citigroup, Goldman Sachs, JP Morgan Chase, And Wells Fargo Saw Their Tax Rates Decline To 22% From About 30% In 2016. According to the New York Times, “The five largest banks in the United States reaped tens of billions of dollars in profits in the first half of the year, thanks in part to a strong economy and to the lingering effects of President Trump’s tax cuts. Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase and Wells Fargo have all seen their tax rates decline to 22 percent or less as a result of the cuts, compared with rates of around 30 percent three years ago, one of the most consistent sources of strength apparent in quarterly earnings reports issued this week.” [New York Times, 7/17/19]

- Lower Tax Rates Helped Banks Offset “Unremarkable Quarterly Performances.” According to the New York Times, “JPMorgan’s tax rate fell to just under 15 percent in this year’s second quarter, although the bank said it would probably inch higher later in the year. Wells Fargo’s tax rate for the quarter was just over 17 percent, and Bank of America’s was 18 percent. The reduced rates helped offset a general decline in Wall Street trading revenue and added some pep to what would have otherwise been unremarkable quarterly performances by most of the banks.” [New York Times, 7/17/19]

New York Times: Citigroup Beat Quarterly Earnings Expectations, “Mostly” Due To Lower Corporate Tax Rates And Stock Buybacks. According to the New York Times, “Citigroup may have gotten the most significant lift from a lower tax rate. The bank’s chief financial officer, Mark Mason, said the strength in Citi’s adjusted per-share earnings — $1.83, higher than Wall Street analysts’ expectations — was mostly a result of the lower rate and of a decline in its outstanding shares. The decline stemmed from Citi’s repurchasing shares.” [New York Times, 7/17/19]

In Just Two Years Since The Tax Law Was Enacted, Big Banks Saved $32 Billion Due To The Corporate Tax Cuts

The Biggest Six Banks Saw Even Bigger Savings From Trump’s Corporate Tax Cuts, Which Totaled $32 Billion Through The First Two Years Of It Being In Effect. According to Bloomberg, “Savings for the top six U.S. banks from President Donald Trump’s signature tax overhaul accelerated last year, now topping $32 billion as the lenders curbed new borrowing, pared jobs and ramped up payouts to shareholders. JPMorgan Chase & Co., Bank of America Corp., Citigroup Inc., Wells Fargo & Co., Goldman Sachs Group Inc. and Morgan Stanley posted earnings this week showing they saved $18 billion in 2019, more than the prior year, as their average effective tax rate fell to 18% from 20%. Bloomberg News calculated the haul by comparing the lower tax rates to what they paid before the law took effect, which averaged 30%.” [Bloomberg, 1/16/20]

2019: The Six Biggest Banks Posted Net Income Of $120 Billion. According to Bloomberg, “The tax savings have spurred the banks to record profit. The six firms posted $120 billion in net income for 2019, inching past 2018’s mark. They had never surpassed $100 billion before the tax cuts.” [Bloomberg, 1/16/20]

Before Trump’s Corporate Tax Cuts They Had Never Made $100 Billion. According to Bloomberg, “The tax savings have spurred the banks to record profit. The six firms posted $120 billion in net income for 2019, inching past 2018’s mark. They had never surpassed $100 billion before the tax cuts.” [Bloomberg, 1/16/20]

BUSINESS SPENDING AND CORPORATE INVESTMENT DROPPED TO THE LONGEST DECLINE SINCE 2009

January 2020: Corporate Investment Was Lower Than At The Time Of The TCJA’s Passage. According to Vox, “Promises that the tax act would boost investment have not panned out. Corporate investment is now at lower levels than before the act passed, according to the Commerce Department. Though employment and wages have increased, it is hard to separate the effect of the tax act from general economic improvements since the 2008 recession.” [Vox, 1/24/20]

Following The TCJA, Corporations Failed To Make Their Promised Investments

FY 2017 – FY 2018: After FedEx’s Founder And CEO Lobbied For Corporate Tax Cuts To Stimulate Capital Investment, FedEx Reduced Its Tax Burden From ~$1.5 Billion To Zero Despite Investing Less Than It Promised In December 2017. According to the New York Times, “In the 2017 fiscal year, FedEx owed more than $1.5 billion in taxes. The next year, it owed nothing. What changed was the Trump administration’s tax cut — for which the company had lobbied hard. The public face of its lobbying effort, which included a tax proposal of its own, was FedEx’s founder and chief executive, Frederick Smith, who repeatedly took to the airwaves to champion the power of tax cuts. ‘If you make the United States a better place to invest, there is no question in my mind that we would see a renaissance of capital investment,’ he said on an August 2017 radio show hosted by Larry Kudlow, who is now chairman of the National Economic Council. Four months later, President Trump signed into law the $1.5 trillion tax cut that became his signature legislative achievement. FedEx reaped big savings, bringing its effective tax rate from 34 percent in fiscal year 2017 to less than zero in fiscal year 2018, meaning that, overall, the government technically owed it money. But it did not increase investment in new equipment and other assets in the fiscal year that followed, as Mr. Smith said businesses like his would.” [New York Times, 11/17/19]

- FY 2017 – FY 2019: FedEx More Than Doubled Its Spending On Stock Buybacks And Dividends As Its Tax Liability Decreased By At Least $1.6 Billion. According to the New York Times, “FedEx’s financial filings show that the law has so far saved it at least $1.6 billion. Its financial filings show it owed no taxes in the 2018 fiscal year overall. Company officials said FedEx paid $2 billion in total federal income taxes over the past 10 years. As for capital investments, the company spent less in the 2018 fiscal year than it had projected in December 2017, before the tax law passed. It spent even less in 2019. Much of its savings have gone to reward shareholders: FedEx spent more than $2 billion on stock buybacks and dividend increases in the 2019 fiscal year, up from $1.6 billion in 2018, and more than double the amount the company spent on buybacks and dividends in fiscal year 2017.” [New York Times, 11/17/19]

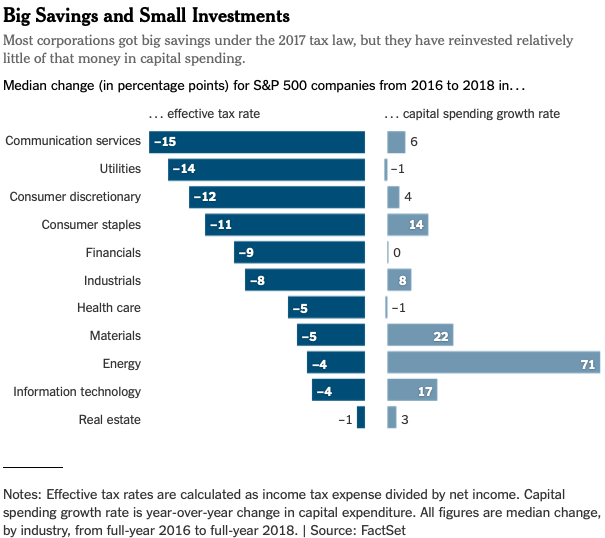

- As S&P 500 Companies Saw Their Effective Tax Rates Fall From 25.9% To 18.1%, They Spent Nearly Three Times As Much On Additional Dividends And Buybacks Than On Increased Capital Investment. According to the New York Times, “FedEx’s use of its tax savings is representative of corporate America. Companies have already saved upward of $100 billion more on their taxes than analysts predicted when the law was passed. Companies that make up the S&P 500 index had an average effective tax rate of 18.1 percent in 2018, down from 25.9 percent in 2016, according to an analysis of securities filings. More than 200 of those companies saw their effective tax rates fall by 10 points or more. Nearly three dozen, including FedEx, saw their tax rates fall to zero or reported that tax authorities owed them money. From the first quarter of 2018, when the law fully took effect, companies have spent nearly three times as much on additional dividends and stock buybacks, which boost a company’s stock price and market value, than on increased investment.” [New York Times, 11/17/18]

A New York Times Analysis Showed Negative Correlation Between Corporate Tax Burden Reduction And Increase In Capital Investment. According to the New York Times, “Nearly two years after the tax law passed, the windfall to corporations like FedEx is becoming clear. A New York Times analysis of data compiled by Capital IQ shows no statistically meaningful relationship between the size of the tax cut that companies and industries received and the investments they made. If anything, the companies that received the biggest tax cuts increased their capital investment by less, on average, than companies that got smaller cuts.” [New York Times, 11/17/19]

[New York Times, 11/17/19]

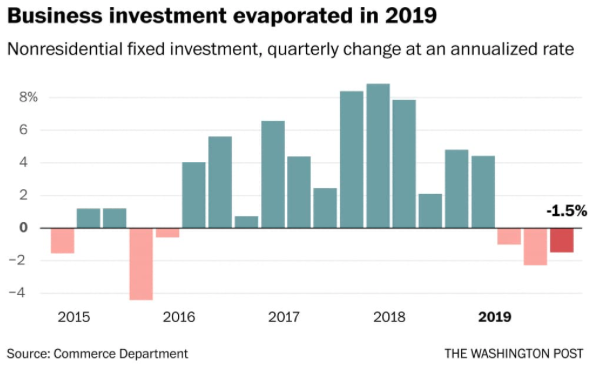

2019: The U.S. Faced An Investment Recession In Addition To A Manufacturing One. According to Bloomberg, “The GDP report included more evidence that the U.S. was plagued by an investment recession as well as a manufacturing one last year. Gross private domestic investment fell 1.9% in the fourth quarter from a year earlier, while investment in non-residential structures fell 7% and equipment was down 1.5%. Kevin Cummins, senior U.S. economist at NatWest Markets, said the slump in imports also appeared to reflect weaker consumer demand, one of the big drivers of the U.S. economy traditionally. ‘If consumption is weakening, you’re going to have weaker imports, which ironically, should be a net positive for top-line GDP,’ he said. ‘But I think it’s a sign of weaker consumer demand more than anything else.’” [Bloomberg, 1/30/19]

Q4 2019: Continued Cutbacks In Business Investment Contributed To The Longest Period Of Investment Decline Since 2009. According to Bloomberg, “The longest pullback in U.S. business investment since 2009 shows little sign of ending, which could weigh further on the economy this year just as the once-gangbusters household spending that had been picking up the slack also slows down. Thursday’s fourth-quarter data on gross domestic product showed steady top-line expansion of 2.1% that reflected a big boost from falling imports and masked a weaker composition of growth. Nonresidential investment fell an annualized 1.5% in the third straight decline, while consumer spending decelerated to a 1.8% gain, below projections after the strongest consecutive quarters since 2015.” [Bloomberg, 1/30/20]

Q4 2019: Core GDP Grew At The Slowest Rate In Four Years, Even As Increased Government Spending Caused A Significant Boost. According to Bloomberg, “Thursday’s data showed a closely watched gauge of underlying demand, which strips out the volatile trade and inventories components of GDP, expanded 1.6% in the quarter. Without government purchases, that number looked even weaker at only 1.4%, the slowest in four years.” [Bloomberg, 1/30/20]

NON-REAL ESTATE SPECIFIC PROVISIONS IN THE TCJA BENEFITTED CORPORATIONS AND THE WEALTHY

Trump’s Tax Plan Global Minimum Tax (GILTI) Policies Cost Revenue Gains

If Trump And Republicans Had Implemented A Per-Country Minimum Tax Instead Of A Global One, U.S. Revenue Gains Would Have Been 2.5 Times Larger. According to a paper by Kimberly A. Clausing published on the Social Science Research Network, “However, the global nature of the minimum tax, in comparison to a per-country minimum tax, substantially reduces its impact. Indeed, the global nature of the minimum tax makes the U.S. the least desirable place to book income for many multinational companies, because if they do not have sufficient foreign tax credits to offset minimum tax due, even high-taxed foreign income is preferable to U.S. income when foreign tax credits shield haven income from the GILTI tax. In contrast, under a per-country minimum tax, reductions in haven tax bases would be about twice as large, and U.S. revenue gains from the minimum tax would be more than two and a half times higher.” [Kimberly A. Clausing – Social Science Research Network, 4, 11/21/18]

Because The First 10% Return On Assets In Foreign Income Is Exempt From Taxation Under The TCJA, Companies Are Incentivized To Move Assets Out Of The Country. According to a Paper by Kimberly A. Clausing published on the Social Science Research Network, “Despite the shift to a territorial system under the TCJA, there are significant provisions under the law that may actually result in a higher net burden on foreign income for U.S. multinational companies. While there is no tax due upon repatriation, there is a minimum tax due currently on global intangible low-taxed income, or ‘GILTI’ income. While the first ten percent return on assets is exempt from the GILTI tax (providing a perverse incentive to increase real investments abroad), profits beyond that amount are taxable at half the U.S. tax rate.” [Kimberly A. Clausing – Social Science Research Network, 14, 11/21/18]

“America Last” Tax Setup Incentivized Companies To Book Profits Offshore

Because The GILTI Rate Was Lower Than The Corporate Rate In The U.S., Companies Were Incentivized To Book As Much Of Their Profit Outside Of The Country As Possible. According to a paper by Kimberly A. Clausing published on the Social Science Research Network, “But will the GILTI provision cause profit to be shifted into the United States? In practice, that outcome is questionable. Because the TCJA uses a global minimum tax, tax obligations in higher tax countries can offset the minimum tax due on haven income. Therefore, companies can blend their haven and non-haven foreign income, reducing or perhaps eliminating payments of U.S. minimum tax, and achieving a lower tax rate than the U.S. rate. While the global minimum tax discourages profit shifting to havens, it is effectively an ‘America last’ tax policy from the perspective of revenue, because both low-tax and high-tax foreign countries are tax-preferred relative to the United States, if a company is in deficit credit position with respect to GILTI income. (That distinction will be discussed shortly.) Indeed, the GILTI acts as a support for the tax revenues of our trading partners, reducing tax competition pressures. That feature may speak in its favor, as argued by Morse (2018), because it helps combat a race to the bottom in corporate tax competition.”[Kimberly A. Clausing – Social Science Research Network, 15, 11/21/18]

December 2019: Trump’s Treasury Department Issued Rules Allowing Companies To Pay Even Less In GILTI

December 2019: The Treasury Released Rules Exposing U.S.-Based Multinational Companies To Less In Taxes. According to the Wall Street Journal, “U.S.-based multinationals will be less exposed to certain U.S. taxes after the Treasury Department issued new rules implementing two major pieces of the 2017 tax law. The regulations, unveiled on Monday, will help ease the burden of two separate minimum taxes that were designed to put a floor under corporate tax collections. Senior Treasury officials said rules largely finalize regulations proposed late last year, while also addressing U.S. multinational firms’ concerns.” [Wall Street Journal, 12/2/19]

- One New Rule Would Allow Companies To Exempt 50% Of Certainty Assets. According to The Wall Street Journal, “One minimum tax affected by the regulations is the Global Intangible Low-Taxed Income tax, or GILTI, which affects U.S.-based companies with foreign operations. It was designed to limit companies’ ability to book profits in low-tax jurisdictions without paying U.S. taxes and was projected to raise $112 billion over a decade. The rule issued Monday includes a provision that would allow companies to treat certain assets as 50% exempt for expense allocation purposes under GILTI, a senior Treasury official said.”[Wall Street Journal, 12/2/19]

- Trump’s Treasury Issued A Rule Giving Companies More Generous Treatment Of Foreign Tax Credits. According to the Wall Street Journal, “Treasury officials also proposed more generous rules for calculating foreign tax credits, including changes to the allocation and apportionment of research and experimental tax deductions. The Treasury official said the change will generally allow those subject to the GILTI tax to increase their use of foreign tax credits, helping companies that conduct research and development in the U.S. The second minimum tax is known as the Base Erosion and Anti-Abuse Tax, which makes it harder for companies to load up their U.S. operations with deductions and push profits to related entities abroad. The tax was projected to raise $150 billion over a decade.” [Wall Street Journal, 12/2/19]

The 20% Pass-Through Deduction Was A Huge Moneymaker For The Trump Organization

Pass-Through Businesses’ Tax Was Paid As An Individual Income Tax Instead Of Corporate Tax. According to Vox, “Pass-throughs are single-owner businesses, partnerships, limited liability companies, (known as LLCs) and special corporations called S-corps. Most real estate companies are organized as LLCs. Trump owns hundreds of them, and the Center for Public Integrity’s analysis found that 22 of the 47 members of the House and Senate tax-writing committees in 2017 were invested in them. Pass-throughs can be found in any industry. They pay no corporate taxes and steer their profits as income to business owners or investors, who are taxed only once at their individual rates. Despite their favored treatment as a business vehicle, the 2017 tax act did them another favor: It allowed 20 percent to be deducted off the top of the pass-through income for tax purposes.” [Vox, 1/24/20]

Trump Alone Owns Hundreds Of Pass-Through Businesses. According to Vox, “Pass-throughs are single-owner businesses, partnerships, limited liability companies, (known as LLCs) and special corporations called S-corps. Most real estate companies are organized as LLCs. Trump owns hundreds of them, and the Center for Public Integrity’s analysis found that 22 of the 47 members of the House and Senate tax-writing committees in 2017 were invested in them. Pass-throughs can be found in any industry. They pay no corporate taxes and steer their profits as income to business owners or investors, who are taxed only once at their individual rates. Despite their favored treatment as a business vehicle, the 2017 tax act did them another favor: It allowed 20 percent to be deducted off the top of the pass-through income for tax purposes.” [Vox, 1/24/20]

Businesses Benefited From The Pass-Through Deduction

The TCJA Allowed, And The Treasury Confirmed, The Ability To Deduct Up To 20% Of Income Through Pass-Through Businesses, Some Trusts, And Some Estates. According to Forbes, “The first deduction is the one that likely brought you to this article: the ‘20% pass-through deduction.’ In its most simple terms, Section 199A grants an individual business owner -- as well as some trusts and estates -- a deduction equal to 20% of the taxpayer's qualified business income.” [Forbes, 1/19/19]

The Pass-Through Deduction Also Applied To Real Estate Investment Trusts (REITs) And Publicly Traded Partnerships (PTPs). According to Forbes, “Once this deduction is computed and limited, as appropriate, it is added to the SECOND deduction offered under Section 199A; one that is every bit as simple as the pass-through deduction is complex: a deduction for 20% of the taxpayer's qualified REIT dividends and publicly traded partnership (PTP) income for the year.” [Forbes, 1/19/19]

- Private Equity Firms Like The Carlyle Group Are Often Traded As PTPs. According to the Carlyle Group’s Website, “Carlyle is a publicly traded partnership, which began trading on the NASDAQ market under the CG ticker symbol on May 3, 2012.” [Carlyle Group, accessed 1/27/20]

Trump’s Tax Cuts Added A Deduction Of Up To 20% On $344 Billion In Income From Real Estate Holdings. According to the Wall Street Journal, “Rental real estate is renowned for its many tax breaks, and the 2017 tax overhaul added a new one. Landlords who want to claim it for 2019 should be planning now, because they may need to send 1099 forms early next year. The benefit is the so-called 199A deduction of 20%. It applies to business income—including rental income—earned by many sole proprietorships, limited-liability companies, partnerships and S corporations. These entities pass through profits and losses directly to their owners’ individual tax returns, instead of paying tax at the corporate level. Lots of Americans hold rental real estate in these types of firms. For 2017, about 20 million filers reported $344 billion in rental income on Schedule E of their individual returns, according to Internal Revenue Service data cited by the National Apartment Association, an industry group.” [Wall Street Journal, 10/18/19]

Ron Johnson Was A Strong Proponent Of The Pass-Through Deduction As He Had Multi-Million Dollar Pass-Through Holdings

Ron Johnson, A Member Of The Senate Finance Committee, Held, With His Wife, Millions Of Dollars Worth Of Pass-Through Corporations, Paying His Household Between $250,000 And $2.1 Million Per Year. According to Vox, “No doubt Johnson, with his wife, held interests that year in four real estate or manufacturing LLCs worth between $6.2 million and $30.5 million, from which they received income that year between $250,000 and $2.1 million, according to his financial disclosure form.” [Vox, 1/24/20]

- 2017: Johnson Was A Staunch Proponent Of The Pass-Through Deduction. According to Vox, “In the Senate, the champion for the pass-through break was Ron Johnson, a Wisconsin Republican who was a Budget Committee member when the tax bill was being written. He argued that because the bill was slated to give big corporations a 14 percent cut in their tax rate, smaller businesses should get a break, too. ‘I just have in my heart a real affinity for these owner-operated pass-throughs,’ he told the New York Times when the Senate was considering the tax bill in November 2017.” [Vox, 1/24/20]

Trump’s Tax Law Helped Increase Private Equity Valuations By By 3 – 17%

Early 2016 – September 2017: Trump Campaigned On Closing The Carried Interest Loophole, A Common Way For Private Equity Firms To Reduce Tax Liability. According to ProPublica, “From early in the 2016 presidential campaign, Donald Trump swore he’d do away with the so-called carried-interest loophole, the notorious tax break that allows highly compensated private-equity managers, real estate investors and venture capitalists to be taxed at a much lower rate than other professionals. ‘They’re paying nothing, and it’s ridiculous,’ Trump said in August 2016. ‘These are guys that shift paper around and they get lucky.’ They were, he concluded, ‘getting away with murder.’ As recently as late September, his chief economic adviser, ex-Goldman Sachs executive Gary Cohn, insisted that the administration was set on closing what’s also referred to as the ‘hedge-fund loophole,’ though hedge funds profit from it less than private-equity firms. ‘The president remains committed to ending the carried interest deduction,’ Cohn told CNBC. ‘As we continue to evolve on the framework, the president has made it clear to the tax writers and Congress. Carried interest is one of those loopholes that we talk about when we talk about getting rid of loopholes that affect wealthy Americans.’” [ProPublica, 11/3/17]

- November 2017: Trump’s Tax Cuts Made No Change To The Carried Interest Loophole. According to Bloomberg, “The House tax bill released Thursday preserves the carried interest tax break—paid to private-equity managers, venture capitalists, hedge fund managers and certain real estate investors—despite President Donald Trump and GOP leaders’ promise to do away with loopholes for the wealthy. When asked about carried interest, Ways and Means member Jim Renacci, an Ohio Republican, confirmed there was no change.” [Bloomberg, 11/2/19]

January 2018: Trump’s Corporate Tax Cuts Were Projected To Increase The Value Of Private-Equity-Owned U.S. Companies By 3-17%. According to the Wall Street Journal, “The values of profitable private-equity-owned U.S. companies should climb between 3% and 17% on average as the law moves to lower the corporate tax rate to 21% from 35% and to give companies the ability to deduct capital spending upfront. Those two provisions are expected to trump the higher cost of debt that will result from the legislation, Hamilton Lane found.” [Wall Street Journal, 1/24/18]

THE TCJA INCLUDED CARVE OUTS FOR REAL ESTATE HOLDINGS

Property Exchanges Were Preserved, Allowing Assets To Be Exchanged Without Capital Gains Liability

While The TCJA Restricted Like-Kind Exchanges, Real Estate Eligibility Was Preserved. According to the Internal Revenue Service, “The Internal Revenue Service today reminded taxpayers that like-kind exchange tax treatment is now generally limited to exchanges of real property. The Tax Cuts and Jobs Act, passed in December 2017, made tax law changes that will affect virtually every business and individual in 2018 and the years ahead. Effective Jan. 1, 2018, exchanges of personal or intangible property such as machinery, equipment, vehicles, artwork, collectibles, patents, and other intellectual property generally do not qualify for nonrecognition of gain or loss as like-kind exchanges. However, certain exchanges of mutual ditch, reservoir or irrigation stock are still eligible. Like-kind exchange treatment now applies only to exchanges of real property that is held for use in a trade or business or for investment. Real property, also called real estate, includes land and generally anything built on or attached to it. […] Properties are of like-kind if they’re of the same nature or character, even if they differ in grade or quality. Improved real property is generally of like-kind to unimproved real property. For example, an apartment building would generally be of like-kind to unimproved land. However, real property in the United States is not of like-kind to real property outside the U.S.” [Internal Revenue Service, 11/19/18]

- A Like-Kind Exchange Allows For Assets To Be Exchanged Without Incurring Capital Gains Liability. According to Investopedia, “A like-kind exchange, sometimes styled as a like kind exchange, is a tax-deferred transaction that allows for the disposal of an asset and the acquisition of another similar asset without generating a capital gains tax liability from the sale of the first asset.” [Investopedia, 09/18/19]

The TCJA Raised The Amount Of Capital Expenses Businesses Could Deduct

The TCJA Allowed Businesses To Deduct The Full Cost Of Qualified Investment, Twice What Was Allowed Under Previous Laws. According to The Tax Foundation, “TCJA allowed businesses to deduct the full cost of qualified new investments in the year those investments are made (referred to as 100 percent bonus depreciation or ‘full expensing’) for five years. Bonus depreciation then phases down in 20 percentage point increments beginning in 2023, and is fully eliminated after 2026. Prior law allowed 50 percent bonus depreciation in 2017, decreasing the percentage in subsequent years and fully eliminating it after 2020.” [Tax Foundation, 2018]

- Full Expensing Allowed Real Estate Developers An Incentive To Build. According to William Wheaton’s Blog at the MIT Center for Real Estate, “For real estate in particular, the expensing of new investment is a huge incentive to build new structures: shopping centers, industrial parks, offices. However, these property markets are not exactly crying out for more investment at present. In particular, retail space finds its demand waning as consumers shift to internet shopping. Industrial space demand has been healthy but a building boom is already underway in the sector. In the office sector, hoteling or co-working, which some believe will lower demand for aggregate space, is causing some discomfiture. Expensing could generate new building construction precisely when more space is not warranted by property fundamentals.” [William Wheaton – MIT Center for Real Estate, accessed 1/27/20]

Regulators Appointed By Trump Allowed Banks To Count Stadium Financing As “Helping The Poor”

Trump Appointed Regulators Ruled Financing For Sports Stadiums In Opportunity Zones Qualified For Tax Breaks. According to Crain’s of New York, “For decades, the U.S. has required banks to steer a portion of their money to people in poor neighborhoods. Now, under proposed rule changes, banks may finance upgrades to sports stadiums, call it helping the poor—and potentially even get a generous tax break. That scenario might seem oddly specific, but it’s what two regulators appointed by President Donald Trump said last week they may allow as they undertake the most significant rewrite of the Community Reinvestment Act in a quarter-century. The agencies drafted a long list hypothetical ways banks could seek to meet their obligations, including this sentence on page 100 of their proposal: ‘Investment in a qualified opportunity fund, established to finance improvements to an athletic stadium in an opportunity zone that is also an LMI census tract.’ (LMI refers to low- or moderate-income.)” [Crain’s of New York, 12/16/19]

2019: 91 CORPORATIONS PAID NOTHING IN FEDERAL INCOME TAXES

Institute On Taxation And Economic Policy: 379 Profitable Fortune 500 Companies Paid Effective Tax Rate Of 11.3%, 54 % Of What They Would Owe On All Reported Profits. According to Yahoo Finance, “Under the Tax Cuts and Jobs Act, 91 profitable Fortune 500 companies paid $0 in taxes on U.S. income in 2018, according to a new report from the Institute on Taxation and Economic Policy (ITEP). Across all 379 profitable companies in the Fortune 500 the effective tax rate was just 11.3%, just over half the 21% tax rate under the law. ‘In 2018, the 379 companies earned $765 billion in pretax profits in the United States,’ the report noted. ‘Had all of those profits been reported to the IRS and taxed at the statutory 21% corporate tax rate, the 379 companies would have paid almost $161 billion in income taxes in 2018.’ Instead, the companies only paid $86.8 billion, roughly 54% of what they owed.” [Yahoo Finance, 12/16/19]

91 Paid Companies $0 In U.S. Income Taxes. According to Yahoo Finance, “Under the Tax Cuts and Jobs Act, 91 profitable Fortune 500 companies paid $0 in taxes on U.S. income in 2018, according to a new report from the Institute on Taxation and Economic Policy (ITEP). Across all 379 profitable companies in the Fortune 500 the effective tax rate was just 11.3%, just over half the 21% tax rate under the law. ‘In 2018, the 379 companies earned $765 billion in pretax profits in the United States,’ the report noted. ‘Had all of those profits been reported to the IRS and taxed at the statutory 21% corporate tax rate, the 379 companies would have paid almost $161 billion in income taxes in 2018.’ Instead, the companies only paid $86.8 billion, roughly 54% of what they owed.” [Yahoo Finance, 12/16/19]

2018 Was One Of The Three Lowest Years Since 1980, Including During The Great Recession, For Corporate Tax Revenue As A Share Of Federal Expenditures. According to the Washington Post, “In the United States, corporate taxes have plunged dramatically as a share of the federal budget, from more than 4 percent to around 1 percent, putting strain on other sources of revenue. Only two other times since 1980 have corporate tax revenue represented such a small share of the federal budget, including in 2009 during the Great Recession.” [Washington Post, 12/16/19]

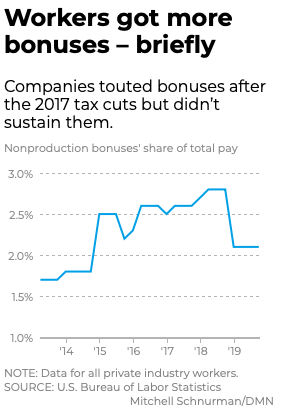

THE BONUSES TOUTED AFTER THE TCJA PASSED WERE ONE-TIME AND INSIGNIFICANT COMPARED TO THE SHAREHOLDER RETURNS

After Trump’s Tax Cuts Passed, Bonuses Spiked, Only To Fall To The Lowest Level In Five Years By September 2019. According to the Dallas Morning News, “After the tax cuts, bonuses for private-sector workers rose almost 12% compared with the third quarter of 2017, according to data from the National Compensation Survey by the U.S. Bureau of Labor Statistics. By late 2018, however, those gains were gone, and employer costs for bonuses had declined 25%. ‘There is zero evidence that the highly-publicized bonuses were any kind of lasting change,’ said Matthew Gardner, a senior fellow at the Institute on Taxation and Economic Policy in Washington. He said it’s too soon to measure some effects of the tax law, given that it’s been in place for only two years and data often lags. ‘But one thing we know is that the bonuses were a temporary thing and not a lasting measure of generosity on the part of these companies,’ Gardner said. After the tax cuts, bonuses rose to 2.8% of total pay, the highest level since at least 2004. That mark held for three quarters, and then the share declined to 2.1%, where it has remained for a year. In September 2019, the most recent period for the BLS data, the share of pay going to bonuses was the lowest in five years.” [Dallas Morning News, 1/14/20]

The Bonuses Paid To Workers After Trump’s Tax Cuts Were Less Than 3% Of The Total Corporate Tax Savings. According to the Dallas Morning News, “The extra cash from tax savings and repatriated funds helped companies invest record sums in buying back their shares. If the tax-cut bonuses topped $4 billion, as one group said, that would be less than 3% of the corporate tax cut and a smaller share of repatriated funds, the Congressional Research Service said.” [Dallas Morning News, 1/14/20]

Despite AT&T’s Promise To Create 7,000 New Jobs Following The TCJA’s Passage, They Have Cut 37,818 Since It Passed

2017: While Lobbying For The TCJA’s Passage, AT&T Promised To Invest $1 Billion And Create 7,000 Jobs. According to ARS Technica, “AT&T in November 2017 pushed for the corporate tax cut by promising to invest an additional $1 billion in 2018, with CEO Randall Stephenson saying that ‘every billion dollars AT&T invests is 7,000 hard-hat jobs. These are not entry-level jobs. These are 7,000 jobs of people putting fiber in ground, hard-hat jobs that make $70,000 to $80,000 per year.’” [ARS Technica, 05/14/19]

January 2018 – January 2020: Since The TCJA Went Into Effect, AT&T Cut 37,818 Jobs As They Cut Capital Spending By $1 Billion. According to The Communications Workers of America, “Today’s AT&T earnings report shows that AT&T continues to cut jobs and reduce capital expenditures even as the company announced record operating and free cash flow for 2019 and more than $5 billion in stock buybacks in the past four months. The company has cut 37,818 jobs since the Tax Cuts and Jobs Act (TCJA) went into effect in 2018, including 4,040 in the fourth quarter of 2019. Capital expenditures declined by more than $1 billion in 2019 as compared to 2018.” [Communications Workers of America, 01/29/20]

Most Corporate Tax Savings Went To Shareholders

2018: American Companies Paid Out More Than $1 Trillion In Stock Buybacks, A Record By More Than $200 Billion. According to CNN, “Corporate America celebrated the first full year under the new tax law by rolling out a record-setting $1 trillion of stock buybacks. US companies, led by Lowe's (LOW) and AbbVie (ABBV), rewarded shareholders by unveiling $34.4 billion in buybacks last week, according to TrimTabs Investment Research. That lifted repurchase announcements above $1 trillion for the first time ever, TrimTabs said, exceeding the prior record of $781 billion set in 2015.” [CNN, 12/17/18]

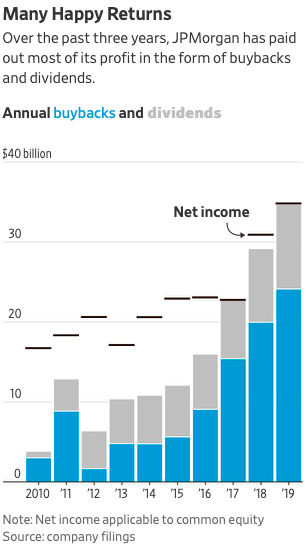

2017 – 2019: JPMorgan Spent 98 Percent Of Its Profits On Buybacks And Dividends. According to the Wall Street Journal, “JPMorgan has paid out $87 billion in buybacks and dividends over the past three years—98% of its profits, roughly in line with rivals. Most of that has been through stock repurchases.” [Wall Street Journal, 2/2/20]

The TCJA Led To An Explosion Of The National Debt

THE TCJA WAS EXPECTED TO ADD $1.9 TRILLION TO $2.2 TRILLION TO THE NATIONAL DEBT

June 2018: Revenue Results From The First Six Months Of The TCJA Lined Up With The Penn Wharton’s December 2017 Projection, Which Said The Legislation Would Add Between $1.9 Trillion And $2.2 Trillion In Debt Over 10 Years. According to the Penn Wharton Budget Model, “In PWBM’s report from December, 2017, we showed that by 2027, even after accounting for economic growth spurred by the TCJA, the overall impact would still result in an increase in debt between $1.9 and $2.2 trillion. By 2040 we show that the deficit would increase between $2.2 and $3.5 trillion. Figure 1 below depicts how the TCJA will impact federal revenues and debt over the next few decades. In fact, as of June 2018 tax receipts met with PWBM projections.” [Penn Wharton Budget Model, 10/18/18]

A STUDY FOUND THAT TRUMP’S TAX CUTS ADDED MORE THAN $100 BILLION A YEAR TO THE NATIONAL DEBT

A Study Concluded That The 2017 Trump Tax Cuts Did Result In Modest Pay Increases For Workers And Investments In The Economy, But Less Than Promised By Republicans And At A Cost Far Exceeding Expectations. According to the New York Times, “The corporate tax cuts that President Donald J. Trump signed into law in 2017 have boosted investment in the U.S. economy and delivered a modest pay bump for workers, according to the most rigorous and detailed study yet of the law’s effects. Those benefits are less than Republicans promised, though, and they have come at a high cost to the federal budget. The corporate tax cuts came nowhere close to paying for themselves, as conservatives insisted they would. Instead, they are adding more than $100 billion a year to America’s $34 trillion-and-growing national debt, according to the quartet of researchers from Princeton University, the University of Chicago, Harvard University and the Treasury Department.” [New York Times, 3/4/24]

The $750 Average Wage Gain Was Far Below The Minimum Promise Of $4,000 Made By Trump Administration Officials. According to the New York Times, “The researchers found the cuts delivered wage gains that were ‘an order of magnitude below’ what Trump officials predicted: about $750 per worker per year on average over the long run, compared to promises of $4,000 to $9,000 per worker. The study is the first to use vast data from corporate tax filings to draw conclusions about the Tax Cuts and Jobs Act, which passed with only Republican support. Its findings could help shape debate on renewing parts of the law that are set to expire or have begun to phase out.” [New York Times, 3/4/24]

The TCJA Raised Taxes On Children Of Deceased Service Members And Students Receiving Financial Aid

THE TCJA ALTERED THE KIDDIE TAX, A PROVISION DESIGNED TO STOP RICH PARENTS FROM GIVING THEIR KIDS MONEY AS TAX AVOIDANCE

1986: Congress Passed The Kiddie Tax As A Way To Prevent Parents From Transferring Wealth To Their Children As A Way To Avoid Taxes. According to the Wall Street Journal, “Congress passed the Kiddie Tax in 1986. Until then a parent could, say, give a child appreciated stock and the child could sell it, pay tax at lower rates, and use the proceeds to pay for college tuition or a Corvette. The 1986 provision levied the Kiddie Tax on a broad range of children’s ‘unearned’ income above an exemption, which currently is $2,200. Above that amount, the children owed tax at the parents’ rate. The levy has never applied to a youngster’s earnings from being a camp counselor or designing websites.” [Wall Street Journal, 5/10/19]

2017: Republicans Changed The Kiddie Tax Rate From The Parent’s Rate To Trust Tax Rates, Resulting In A 37% Tax On Income Over $12,751. According to the Wall Street Journal, “Many features of the 1986 Kiddie Tax were complex, however. To simplify, the 2017 overhaul switched the Kiddie Tax rate from the parents’ rate to trust tax rates. These kick in at a very low level of taxable income: For 2019, the top rate of 37% takes effect at just $12,751.” [Wall Street Journal, 5/10/19]

THE TCJA RAISED TAXES ON AS MANY AS 10,000 CHILDREN OF DECEASED SERVICE MEMBERS

2018: After The Death Of Her Husband, Rebecca Headings Paid A Top Rate Of 12 Percent On Her $55,000 In Income. Her Son Paid 37% On His $29,300 In Annual Survivor’s Benefit. According to the Wall Street Journal, “Rebecca Headings’s husband, U.S. Navy Senior Chief Petty Officer Gary Headings, died of a heart attack at age 39 in 2017. After Mr. Headings’s death, his son began getting an annual survivor’s benefit paid to many families who have lost active-duty service members—often called Gold Star families. Last year, that benefit was about $29,300. But his son, age 6, owed nearly $7,000 in federal taxes on it. ‘At first I was stunned, and then angry. My child’s tax rate is higher than mine,’ says Ms. Headings, a social worker in Virginia Beach. Ms. Headings’s top rate on her 2018 income of less than $55,000 was 12%. Her son’s top rate is 37%. In past years, her son’s tax bill would have been far lower. But a 2017 change to the so-called Kiddie Tax often boosts rates on ‘unearned’ income received by children of middle- and low-income families—including her son.” [Wall Street Journal, 5/10/19]

- As Many As 10,000 Children As In The Same Position As Headings’ Son. According to the Wall Street Journal, “But a revision to the tax in the big overhaul passed by Congress in 2017 is raising taxes on as many as 10,000 children of deceased service members who earn an average annual benefit of about $13,000, according to Department of Defense data provided by the Tragedy Assistance Program for Survivors, or TAPS. It’s a nonprofit group for families who have lost service members that’s working to change the law.” [Wall Street Journal, 5/10/19]

UNDER THE TCJA, FINANCIAL AID PROVIDED BY COLLEGES IS TAXABLE UNDER THE KIDDIE TAX

College Students From Low-Income Families Who Receive Financial Aid Technically Owed Taxes On It At Trust Rates Under The TCJA’s Kiddie Tax. According to the Wall Street Journal, “The Kiddie Tax revision also threatens college students from lower-income families who receive financial aid for expenses other than tuition and supplies. By law such income is taxable, says Tim Steffen, a tax specialist with Robert W. Baird & Co. If a family is in a low tax bracket, then a child receiving taxable aid could wind up in a much higher bracket—with no money to pay the tax. Mark Kantrowitz, the publisher of Savingforcollege.com, estimates that more than three million students could be affected.” [Wall Street Journal, 5/10/19]

- While The IRS Has Not Enforced This Aspect Of The TCJA, The Fact That It Can Has Created Significant Uncertainty For Financial-Aid Providers. According to the Wall Street Journal, “The Kiddie Tax revision isn’t yet a disaster for some of these students for two reasons. Colleges aren’t currently required to report taxable aid to the Internal Revenue Service, and many don’t. Also, the IRS doesn’t seem to be enforcing the law in this area, tax specialists say. Still, the law is on the books. Financial-aid providers are alarmed and are pushing to make scholarships tax-free. Robert Ballard heads Scholarship America, a nonprofit that distributed $264 million to 104,000 students last year. He says, ‘College scholarships are to help students get higher education, but the 2017 Kiddie Tax change is pulling in the opposite direction.’” [Wall Street Journal, 5/10/19]

The TCJA Provided Extensive Benefits To The Rich

ENOUGH OF THE TCJA’S BENEFITS FLOWED TO THE RICHEST AMERICANS TO MAKE THE TAX CODE NO LONGER PROGRESSIVE AT EXTREME INCOME LEVELS

By 2027, The Average Tax Cut Under The TCJA Would Be $160 And 99% Of The Benefit Would Go To The Top 5% Of Earners. According to the Tax Policy Center, “In 2027, the overall average tax cut would be $160, or 0.2 percent of after-tax income (table 3), largely because almost all individual income tax provisions would sunset after 2025. On average, taxes would be little changed for taxpayers in the bottom 95 percent of the income distribution. Taxpayers in the bottom two quintiles of the income distribution would face an average tax increase of 0.1 percent of after-tax income; taxpayers in the middle income quintile would see no material change on average; and taxpayers in the 95th to 99th income percentiles would receive an average tax cut of 0.2 percent of after-tax income. Taxpayers in the top 1 percent of the income distribution would receive an average tax cut of 0.9 percent of after-tax income, accounting for 83 percent of the total benefit for that year.” [Tax Policy Center, 12/18/17]

- Moody’s: Trump’s Tax Cut Bill “Will Contribute To The Widening Of The U.S.’s Inequality By Exacerbating Income And Wealth Concentration.” According to Yahoo Finance, “The tax cuts gave some relief to the middle class, and more is supposed to trickle down from the business sector as corporate tax cuts boost profits and leave more money for investing. But Moody’s doesn’t see that happening, because tax cuts were bigger for higher earners, who also benefit disproportionately from a reduction in the corporate tax rate from 35% to 21%. ‘The Tax Cuts and Jobs Act will contribute to the widening of the U.S.’s inequality by exacerbating income and wealth concentration,’ Moody’s’ concludes. ‘Overall, the tax reform disproportionately benefits households with high incomes and very high levels of wealth.’” [Yahoo Finance, 10/8/18]

- Under Trump’s Tax Law, A Household Earning $348,000 Saw A $10,000 Boost In After-Tax Income, While Earners In The Bottom 20% Saw An Average Boost Of Just $56. According to CBS News, “The rich are getting richer thanks to the tax bill -- and even faster than before. The top 20 percent of earners around the country have seen a nearly 3 percent gain in after-tax income since the tax cuts were passed a year ago, according to the Tax Policy Center. That means a typical household in that group, which has annual income of roughly $348,000, will enjoy a boost of about $10,000. Meanwhile, income for the lowest 20 percent of earners rose only 0.4 percent after the tax bill -- that amounts to a benefit of $56. After-tax income for middle-class Americans -- those in the middle 60 percent -- increased between 1.2 and 1.9 percent this year.” [CBS News, 12/21/18]

FY 2018: Tax Refunds For Households Taxpayers Earning Between $250,000 And $500,000 Increased By An Average Of 11%. According to the Wall Street Journal, “The fresh data shows that while refund statistics barely budged for lower- and middle-income workers, real movement occurred toward the upper end of the income distribution. Average refunds for taxpayers making between $100,000 and $250,000 dropped 10%, while average refunds for those between $250,000 and $500,000 rose by 11%.” [Wall Street Journal, 7/2/19]

Under The TCJA, For The First Time In History, The Richest Households Paid Lower Taxes Than Others

2018: For The First Time On Record, The 400 Richest American Households Payed A Lower Tax Rate Than Any Other Income Group. According to an opinion piece by David Leonhardt in the New York Times, “For the first time on record, the 400 wealthiest Americans last year paid a lower total tax rate — spanning federal, state and local taxes — than any other income group, according to newly released data.” [David Leonhardt-New York Times, 10/6/19]

- Trump’s Tax Cuts Built On The Trend Of Cutting Taxes For The Super-Rich To The Point Where They Paid Less Than Any Other Group. According to an opinion piece by David Leonhardt in the New York Times, “That’s a sharp change from the 1950s and 1960s, when the wealthy paid vastly higher tax rates than the middle class or poor. Since then, taxes that hit the wealthiest the hardest — like the estate tax and corporate tax — have plummeted, while tax avoidance has become more common. President Trump’s 2017 tax cut, which was largely a handout to the rich, plays a role, too. It helped push the tax rate on the 400 wealthiest households below the rates for almost everyone else.” [David Leonhardt-New York Times, 10/6/19]

- 1950 – 2018: The Overall Tax Rate On The Richest 400 Households Declined By Almost 70%, Declining By More Than Half Since 1980, Even As Middle Class Families Saw Almost No Change. According to an opinion piece by David Leonhardt in the New York Times, “The overall tax rate on the richest 400 households last year was only 23 percent, meaning that their combined tax payments equaled less than one quarter of their total income. This overall rate was 70 percent in 1950 and 47 percent in 1980. For middle-class and poor families, the picture is different. Federal income taxes have also declined modestly for these families, but they haven’t benefited much if at all from the decline in the corporate tax or estate tax. And they now pay more in payroll taxes (which finance Medicare and Social Security) than in the past. Over all, their taxes have remained fairly flat. The combined result is that over the last 75 years the United States tax system has become radically less progressive.” [David Leonhardt-New York Times, 10/6/19]

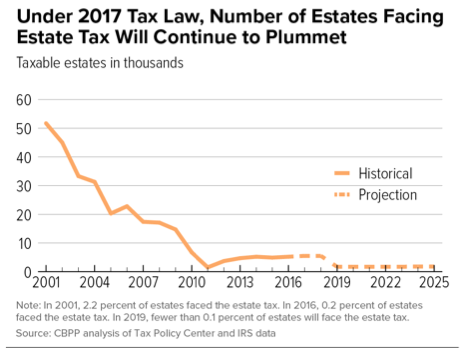

DOUBLING OF THE ESTATE TAX EXEMPTION SAVED THE 1,800 LARGEST ESTATES $4.4 MILLION EACH

The TCJA Doubling Of Estate Tax Exemption Would Exempt All But 1,800 Households, And Give Each Of Those Households A Tax Cut Of $4.4 Million Each. According to the Center on Budget And Policy Priorities, “The 2017 tax law doubles the amount of an estate’s value that’s exempt from the estate tax, from $11 million per couple ($5.5 million per individual) to $22 million per couple ($11 million per person). That will: Reduce the share of estates facing the tax to fewer than 1 in 1,000. Even before the tax law was enacted, only the wealthiest 2 in 1,000 estates faced the estate tax. Policymakers have dramatically raised the exemption level in recent decades (from $675,000 per person in 2001), so very few estates are large enough to be taxable. Now only the largest 1,800 estates each year will face the estate tax. Give each of the 1,800 very largest estates a tax cut of $4.4 million per couple. Doubling the exemption will eliminate the estate tax for estates worth between $11 million and $22 million per couple, and give the remaining 1,800 estates worth over $22 million per couple a tax cut of $4.4 million (40 percent of the additional $11 million in assets that would be exempt).” [Center on Budget and Policy Priorities, 6/1/18]

- Large Inheritances Accelerated Growing Wealth Inequality And Discouraged Heirs From Working. According to the Center on Budget and Policy Priorities, “The estate tax is the most progressive part of the U.S. tax code because it affects only those who are most able to pay. Large inheritances play a significant role in the concentration of wealth; inheritances account for about 40 percent of all household wealth and are extremely concentrated at the top. Weakening the estate tax, therefore, exacerbates wealth inequality. Proponents of cutting the estate tax argue it will help non-wealthy Americans by increasing growth, but cutting it likely has little or no impact on wealthy donors’ savings and actually discourages wealthy heirs from working. The estate tax is an efficient way to raise revenue without imposing burdens on low- and middle-income Americans.”[Center on Budget and Policy Priorities, 6/1/18]

THE TCJA’S CHILD TAX CREDIT SKEWED TOWARDS THE WEALTHY

Trump’s Tax Cuts Expanded The Child Tax Credit To Families Earning As Much As $400,000 Per Year. According to the New York Times, “The 2017 tax bill, President Trump’s main domestic achievement, doubled the maximum credit in the two-decade-old program and extended it to families earning as much as $400,000 a year (up from $110,000).” [New York Times, 12/16/19]

- 35% Of Children Would Not Get The Full Amount Because Their Parents Did Not Earn Enough. According to the New York Times, “While Republicans say the increase shows concern for ordinary families, 35 percent of children fail to receive the full $2,000 because their parents earn too little, researchers at Columbia University found. A quarter get a partial sum and 10 percent get nothing. Among those excluded from the full credit are half of Latinos, 53 percent of blacks and 70 percent of children with single mothers.” [New York Times, 12/16/19]

- A Single Mother Of Two Would Need To Earn More Than $30,000 To Receive The Full Credit. According to the New York Times, “Because the credit rises with earnings, a single parent with two children has to earn more than $30,000 a year to collect the full amount.” [New York Times, 12/16/19]

- Even As Trump’s Tax Cuts Gave Upper-Income Families Access To $2,000 Per Child, While Full-Time Minimum Wage Workers Received Just $75. According to the New York Times, “By enriching the credit and including the affluent, the Trump expansion itself has brought attention to the poor children it excludes. While the 2017 law made millions of upper-income families eligible for the $2,000 credit (in part to offset the loss of other tax benefits), it gave a boost of just $75 to most full-time workers at the minimum wage.” [New York Times, 12/16/19]

THE IRS SAW DECLINING AUDIT RATES

2019: The IRS Missed Out On Billions Of Dollars In Revenue As Only .45% Of Personal Income Tax Returns Were Audited, Less Than Half Of The 1.1% In 2010. According to the Wall Street Journal, “Individual taxpayers are half as likely to get audited as they were in 2010, after tax enforcement by the Internal Revenue Service fell to the lowest level in at least four decades. The IRS audited 0.45% of personal income-tax returns in fiscal 2019, down from 0.59% in 2018 and marking the eighth straight year of decline, according to a report released on Monday. In 2010, the IRS audited 1.1% of tax returns. The report doesn’t break down audits by income category or provide details about how much revenue they generate. The steady erosion of tax enforcement has been driven by years of cuts in the agency’s budget along with a heavier workload. The result, according to tax experts, is that the Treasury is letting billions of dollars annually go uncollected, even as budget deficits rise.” [Wall Street Journal, 1/6/20]

Greater Tax Enforcement Could Generate About $1 Trillion In Revenue Over A Decade, As Each Dollar Spent On Enforcement Yields About $4 In Additional Revenue. According to the Wall Street Journal, “Investing in enforcement and tightening rules could generate about $1 trillion over a decade, according to Harvard University economist Lawrence Summers, who served as Treasury secretary in the Clinton administration, and University of Pennsylvania professor Natasha Sarin. The government estimates that each additional dollar spent on tax enforcement could yield more than $4 in revenue, and Democratic presidential candidates have made increasing IRS funding part of their agenda. The IRS budget is about 20% below the 2010 peak in inflation-adjusted dollars, according to the Congressional Budget Office. During that time, Congress has given the agency more responsibility, including the implementation of the 2010 health care law and the 2017 tax law.” [Wall Street Journal, 1/6/20]

TRUMP WANTED TO EXTEND THE 2017 TAX CUTS, WHICH WOULD AGAIN REWARD THE WEALTHIEST AMERICANS

Trump Said Extending The 2017 Tax Cuts Was A Core Issue To His Campaign. According to CNN, “At the dinner, hosted by billionaire investor John Paulson, Trump told the crowd that one of his core issues for a second term would be extending the sweeping tax cuts that congressional Republicans approved in 2017. While the Tax Cuts and Jobs Act reduced taxes for most Americans, the rich benefited far more than others. […] The fate of the 2017 law’s individual tax provisions, which are set to expire at the end of next year, will depend on which party wins control of the White House and Congress in November.” [CNN, 4/10/24]

Tax Policy Center: Millionaires Would Get A 2.3% Tax Cut, While The Lowest Wage Earners Would Only See A .5% Cut. According to CNN, “If they are extended, more than 60% of the benefits would go to those in the top 20% of income, according to the Tax Policy Center, a nonpartisan research group. More than 40% of the benefits would go to those in the top 5%. If Trump achieves his goal, those making between $400,000 and $1 million would get an average tax cut of about $15,000, lifting their after-tax incomes by 3.1%, according to the center’s estimates. Those who earn $1 million or more would enjoy an average tax cut of about $50,000, raising their after-tax incomes by 2.3%. Only about a quarter of those in the lowest income households would see their taxes reduced. Their tax cut would be $100, on average, which would bump up their after-tax incomes by 0.5%.” [CNN, 4/10/24]

TRUMP TOLD BILLIONAIRES HE WOULD KEEP THEIR TAXES LOW

Trump Emphasized He Would Keep Billionaire’s Taxes Low. According to NBC News, “Former President Donald Trump emphasized the importance of extending his signature tax cuts to some of the nation’s wealthiest political donors, according to a readout of his private remarks Saturday night provided by a Trump campaign official. ‘Trump spoke on the need to win back the White House so we can turn our country around, focusing on key issues including unleashing energy production, securing our southern border, reducing inflation, extending the Trump Tax Cuts, eliminating Joe Biden’s insane [electric vehicle] mandate, protecting Israel, and avoiding global war,’ the campaign official said of a roughly 45-minute speech to donors in Palm Beach, Florida.” [NBC News, 4/8/24]

¶ Trump Lied About The Size And Impact Of His Tax Cuts

Despite His Claims To The Contrary, Trump’s Tax Cuts Were Not The Biggest And Did Not Benefit Low-Income People The Most. According to PolitiFact, “‘I gave the biggest tax cuts in the history of our country, bigger than the Ronald Reagan tax cuts (and the) people that benefited the most were low income people.’ Both parts of this statement are wrong. The part about the biggest tax cut is a falsehood that Trump shared repeatedly during his presidency. (Our colleagues at the Washington Post Fact Checker found that this was Trump’s second-most-commonly repeated false claim, shared 295 times during his presidency.) In inflation-adjusted dollars, the tax bill Trump signed was the fourth-largest since 1940, and as a percentage of GDP, it ranked seventh. Meanwhile, the part about low-income taxpayers benefiting more ‘is not correct,’ based on modeling from the Urban Institute-Brookings Institution Tax Policy Center and other think tanks, John Buhl, the Tax Policy Center’s communications director, told PolitiFact earlier this month. The Tax Policy Center analysis found that the Trump-signed legislation would, on average, cut taxes for households in each income group, but that taxpayers in higher-income households would see the biggest benefits.” [PolitiFact, 5/8/24]

The TCJA Was Expected To Cut American Home Values By About 4% Over Seven Years

BY INCREASING TAXES ON HOMEOWNERS AND PUTTING UPWARD PRESSURE ON INTEREST RATES, THE TCJA HIT HOME VALUES

Increased Taxes On Homeowners And Higher Deficits Caused By Trump’s Corporate Tax Cuts Lead To 4 Percent Reduction In Home Prices Over Seven Years (Average Outstanding Mortgage Length). According to ProPublica, “Here’s how it works. Zandi took what financial techies call the ‘present value’ of the property tax and mortgage interest deductions that homeowners will lose over seven years (the average duration of a mortgage) because of changes in the tax law and subtracted it from the value of the typical house. That results in a 3% decline in national home values below what they would otherwise be. The remaining one percentage point of value shrinkage, Zandi says, comes from the higher interest rates that he says will result from the higher federal budget deficits caused by the tax bill. He estimates that rates on 10-year Treasury notes, a key benchmark for mortgage rates, will be 0.2% higher than they would otherwise be, which in turn will make mortgage rates 0.2% higher. Even though interest rates on 10-year Treasury notes are at or near record lows as I write this, they would be even lower if the Treasury were borrowing less than it’s currently borrowing to cover the higher federal budget deficits caused by Trump’s tax bill. If Zandi’s interest-rate take is correct — it’s true by definition, if you believe in the law of supply and demand — even homeowners who aren’t affected by the inability to deduct all their real estate taxes and mortgage interest costs are affected by the tax bill. How so? Because higher interest rates for buyers translate into lower prices for sellers and therefore produce lower values for owners.” [ProPublica, 10/10/19]

- Moody’s Analytics: U.S. Home Prices Declined 4 Percent, $1.04 Trillion, Relative To What They Would Be Without Trump’s Corporate Tax Cuts. According to ProPublica, “Zandi says that because of the 2017 tax law, U.S. house prices overall are about 4% lower than they’d otherwise be. The next question is how many dollars of lost home value that 4% translates into. That isn’t so hard to figure out if you get your hands on the right numbers. Let me show you. The Federal Reserve Board says that as of March 31, U.S. home values totaled about $26.1 trillion. Apply Zandi’s 4% number to that, and you end up with a $1.04 trillion setback for the nation’s home owners. That’s right — a trillion, with a T. Please note that Zandi isn’t saying that house prices have fallen by an average of 4%. That hasn’t happened. What he’s saying is that on average, house prices are about 4% lower than they’d otherwise be.” [ProPublica, 10/10/19]

- The Reduction In Home Price Value Due To Trump’s Corporate Tax Cuts Has Reduced Americans’ Home Equity By 6.6 Percent. According to ProPublica, “Given that the Fed statistics show that homeowners’ equity was $15.76 trillion as of March 31, Zandi’s numbers imply that homeowners’ equity is down about 6.6% from where it would otherwise be. (That’s the $1.04 trillion value loss divided by the $15.76 trillion of equity.)” [ProPublica, 10/10/19]

More Than A Million Military Members Would Be Forced To Participate In Trump’s Payroll Tax Deferral And Then Pay That Money Back In Q1 Of 2021

UNLIKE CIVILIAN GOVERNMENT WORKERS, MEMBERS OF THE MILITARY WILL HAVE NO CHOICE BUT TO PARTICIPATE IN TRUMP’S PAYROLL TAX DEFERRAL

Defense Finance And Accounting Office: Automatic Enrollment In The Deferral Cannot Be Superceded, Unlike For The Majority Of Civilian Government Employees. According to the Military Times, “It’s a deferral of the payroll tax, designed to put more money into the pockets of employees, at least temporarily, in an effort to ease some economic problems caused by the COVID-19 pandemic, according to the Trump memo. But as of pay periods starting Jan. 1, service members (and all employees affected) will repay the money over a four-month period ending April 30. Trump’s memo does require the Secretary of the Treasury to explore ways — including legislation — to eliminate the requirement to repay those taxes. But as of now, the money will have to be repaid. Military members and civilian employees can’t opt out of the deferral; it happens automatically, according to the Defense Finance and Accounting Office. Most federal agencies appear to be participating in the payroll tax deferrals, requiring their employees to take the tax deferral, according to a letter from Everett B. Kelley, national president of the American Federation of Government Employees, to Office of Management and Budget Director Russell Vought. He urged the administration to allow federal workers to choose whether they wanted the tax deferral, or prefer to opt out. Reports are that few civilian employers are choosing to participate in the payroll tax cut deferral program.” [Military Times, 9/8/20]

- More Than A Million Military Members Would Be Subject To The Program. According to the Military Times, “More than a million military members earning $8,666.66 or less per month will see their paychecks increase by 6.2 percent of their basic pay beginning with the mid-September paycheck — but get ready for the bite out of your paycheck when you have to pay it back starting in January. This affects all enlisted members, virtually all warrant officers and many officers, to include everyone up through the grade of O-4. Officers in the grade of O-5 with less than 16 years of service, and those in the grade of O-6 with less than 14 years of service are affected. Those who earn more than $8,666.66 a month will not have their Social Security taxes deferred — they’ll continue to pay the payroll taxes. The increase, for the months of September through December, comes from a Social Security payroll tax deferral put into place by President Donald Trump’s Aug. 8 memorandum, and subsequent Internal Revenue Service guidance.” [Military Times, 9/8/20]

BECAUSE TRUMP DID NOT HAVE THE AUTHORITY TO FORGIVE THOSE TAX OBLIGATIONS, MEMBERS OF THE MILITARY WOULD OWE ALL DEFERRED TAXES

January 2021 – March 2021: A Service Member Who Earned $8,666.66 Per Month In 2020 Would Pay An Additional $537.33 Per Month In Payroll Taxes. According to the Military Times, “For example: A service member earning $8,666.66 per month would see an increase of $537.33 per month in take-home pay during the September-December payroll tax deferral, or $268.67 per pay period. DFAS officials haven’t yet determined how much will be collected per paycheck starting in January. But if the same schedule is followed as during the deferrals through December, that service member would be paying back the same amount per pay period. With the raise, the net effect would be less of a bite per paycheck, depending on the tax bracket.” [Military Times, 9/8/20]

Trump Campaigned On Making The 2017 Tax Cuts Permanent

TRUMP CAMPAIGNED ON MAKING THE TAX CUTS PERMANENT

Trump Planned On Making The 2017 Tax Cuts Permanent

Trump Planned To Make The 2017 Tax Cuts Permanent. According to Bloomberg, “Donald Trump plans to make permanent the 2017 individual tax cuts that he enacted as president while keeping corporate tax levels unchanged in an appeal to working and middle class voters should he retake the White House, according to people familiar with the matter.” [Bloomberg, 1/6/24]

The Tax Cuts For Individuals Were Set To Expire In 2025. According to Bloomberg, “While the 21% tax rate is permanent, his 2017 tax cuts for individuals are set to expire after 2025. Those cuts overwhelmingly benefit wealthy households, small business owners and those in the real estate industry.” [Bloomberg, 1/6/24]

Trump’s Preference Was To Keep The Corporate Tax Rate At 21%, Despite Wanting To Move It To 15% During His Presidency. According to Bloomberg, “Trump’s preference to keep the 21% corporate rate marks a shift from his desire while president to lower the corporate rate to 15%, which generated opposition from both Republicans and Democrats.” [Bloomberg, 1/6/24]

¶ Trump Sought To Extend His Tax Cuts For The Wealthiest Americans

Trump Wanted To Extend His For The Highest Income Brackets. According to the Washington Post, “Trump’s team is focused also on preserving his 2017 tax cuts — including at the higher brackets, a split with Biden. Any extension of any of the cuts would require congressional approval because much of that law is due to expire next year. He has also touted cutting taxes for working-class families and small businesses.” [Washington Post, 6/27/24]

Making The 2017 Tax Cuts Permanent Would Add Trillions To The National Deficit

Trump’s Plan To Make The 2017 Tax Cuts Permanent Would Add Trillions Of Dollars To The National Deficit. According to ABC News, “The revenue generated by a sweeping set of tariffs would allow the Trump administration to reduce taxes for individuals and companies, the Trump campaign said in February. But the details of a tax cut proposal remain uncertain, Moore said. ‘This is all in motion,’ Moore added. ‘Nothing has been decided.’ Trump is committed, however, to extending the tax cuts signed into law during his first term when they begin to phase out in 2025, Moore added. ‘He clearly wants to make sure the tax rates don't go up as they're supposed to do if they let his tax plan expire,’ Moore said. However, a recent report by the nonpartisan Congressional Budget Office, or CBO, said that making permanent the provisions of the Tax Cuts and Jobs Act of 2017 would add $3.5 trillion to the nation's deficit. The U.S. currently holds roughly $31.4 trillion in debt. In a report in February, the CBO projected the federal debt will grow nearly $20 trillion by the end of 2033. ‘Extending the tax cuts would only worsen the already deep budget deficit problem that we're dealing with,’ Blinder said.” [ABC News, 1/6/24]

¶ Wall Street Billionaires Lined Up Behind Trump Because He Promised To Cut Taxes